‘The sight and sound give me PTSD’: Hassles outweigh savings for some car-sharing users

Amid high COE premiums, the programme Talking Point finds out how viable car-sharing is as a transport option and what the user experience is like.

Car-sharing revenue in Singapore is expected to rise by almost 50 per cent to more than S$300 million in four years’ time.

- Car ownership becomes cheaper than car-sharing only if one drives 100 km daily, said an analyst.

- Car-sharing, however, has its inconveniences. Some users have had to remove food stains, for example.

- Out-of-pocket cost increases exponentially when accidents occur, owing to an insurance clause.\

SINGAPORE: As with most car-sharing users, she began trying out this transport option because “cars are so expensive (to own) in Singapore”.

But after she was involved in a minor accident, Jane, who wishes to remain anonymous, has sworn off the concept.

She is among users who answered Talking Point’s call on Instagram to share their experiences. Poor cleanliness, inflexible scheduling and “predatory” insurance practices came up as top concerns.

Car-sharing platforms and rental companies, however, have reported a rise in demand for their services. By 2027, car-sharing revenue in Singapore is expected to rise by almost 50 per cent to S$303 million, according to Statista.

In fact, user penetration in Singapore, at around 7 per cent, is one of the world’s highest at a national level, according to transport analyst Prateek Bansal from Future Cities Lab Global. This comes amid skyrocketing Certificate of Entitlement (COE) premiums.

For users who drive less than 20 kilometres daily, car-sharing would cost “slightly above” S$500 a month, whereas owning a car is thrice as costly, Bansel’s research found. Car ownership becomes economical only if one drives 100 km daily.

But is the cost saving to car-sharing users worth it?

PET FUR, AND A CONDOM

Some users saw cockroaches and termites. One of them found a condom, and another was greeted by animal fur on the seats of their pre-booked car.

“To manage this problem, we always carry Clorox wipes, essential oils and trash bags,” said one user.

Talking Point host Steven Chia tried out car-sharing for a week and began every drive by wiping the car down even as it ate into his rental time.

While a dusty dashboard may be expected, or even food stains, his car smelled of cigarette smoke on one occasion, which made him “nauseous”.

Car-sharing company GetGo said it depends on customers to look after the vehicles.

With a 30-member cleaning crew, the company cleans the cars on a “usage basis”, that is, based on how many customers used the cars, said chief operating officer Chan Jun Kai.

“It can be as soon as a week or sometimes even two weeks,” he said. “With 2,000 vehicles in our fleet, we can’t be cleaning after every booking.”

To deter irresponsible users, GetGo tracks user behaviour by the cleanliness rating provided by the subsequent user of the car. Users who actively dirty vehicles will be removed from the platform, added Chan.

THE FIRST AND LAST MILE HITCHES

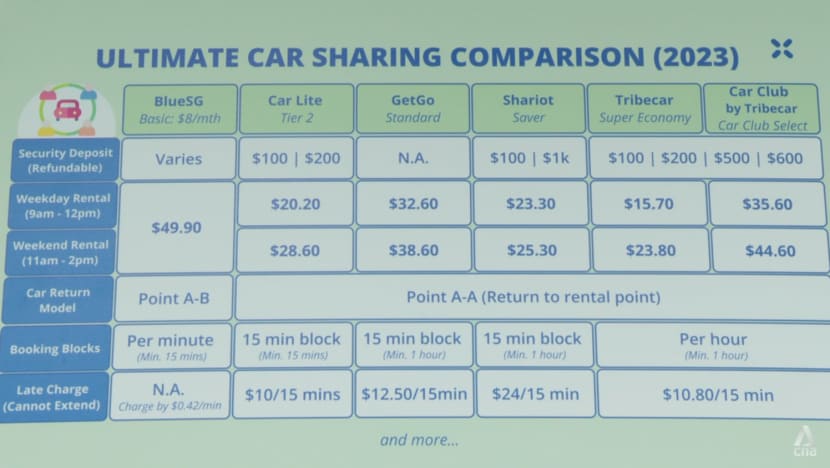

Planning where to pick up and drop off the car is another hassle. Among the providers, BlueSG has different pick-up and drop-off points across Singapore. GetGo, Shariot and Tribecar utilise a Point A-to-A system.

The pick-up points of any service nearest to Chia were at least 1.7 kilometres from his home — a short bus ride or 25-minute walk away. For him, car-sharing may not be viable if his schedule changes at the last minute.

A car may also be unavailable, especially if demand is high on a rainy day. Thus, users are encouraged to make a booking early to secure a car.

Users might also have to stop for fuel if the previous user did not leave much in the tank. This is why car-sharing companies encourage users to fill up the tank when the fuel gauge falls beneath the quarter mark.

The petrol is fully paid for by the company either via a fuel card in the car or via reimbursement with a valid receipt. GetGo also rewards users with promo codes — the amounts vary depending on how full the tank is — while Tribecar users are given their last hour of use for free.

But perhaps more important to some users is avoiding the late charge when returning the car. Fees can range from S$10 per 15 minutes (Car Lite) to S$24 per 15 minutes (Shariot), according to a cost comparison made by Seedly.

One BlueSG user said the company’s charge-per-minute model could make users “more accident-prone”. “When I’m driving BlueSG, all I’m thinking of is speeding till I get to my destination and locking the car,” she said.

THE INSURANCE PITFALL

When accidents happen, however, car-sharing quickly becomes a costly affair owing to an accident insurance clause that dictates excess fees. An excess on an insurance policy is the amount one must pay towards the cost of a claim.

In the event of an accident with a third party, car-sharing users are liable for two excess fees: For their rented car and the third-party claim.

Car owners can usually top up their motor insurance premiums so as not to pay this out-of-pocket cost. But the automatic insurance for car-sharing users involves excess fees ranging from about S$1,000 to more than S$10,000, depending on the user’s age and driving experience.

One BlueSG user, Malcolm Chen, 35, had to pay S$11,250 following an accident in 2021 — his car had crashed into the rear of a vehicle at a traffic light junction.

The other vehicle had a damaged back bumper and a “wonky” exhaust, while his car had a cracked windshield, a damaged front-right bumper, a detached speedometer and two airbags deployed.

A BlueSG representative told him that he would incur “the first-party and third-party liability charges”. But when he asked for a breakdown of the fees, he did not get one.

“I received a lawyer’s letter chasing for payment. I said, ‘Fine, I’ll pay,’” said Chen, who has been driving for 12 years. “Still, no breakdown (was given).”

In response to queries about transparency in car-sharing charges, BlueSG told Talking Point: “We’re always willing to explain our charges and explain what repairs are done. Our claims team handling the accident repairs do explain them to the affected members.”

The issue for Jane is the “crazy amounts” car-sharing providers quote for accidents in the first place.

She said the accident she had last year resulted in “minor” damages to one headlight and bumper of her shared car, along with the other vehicle’s rear bumper.

It was enough to make her liable for a five-figure sum for damage repairs, third-party excess fees and administrative costs.

The third-party excess, quoted in an email to her seen by Talking Point, was between S$5,000 and S$8,000, pending confirmation by the car-sharing provider’s insurer.

“It was a very tiring process, and we also sought legal help (from) free legal clinics just to understand what we can do in such situations,” said Jane, who is in her 30s and has five years of driving experience.

She added that the sight and sound of these cars now “give (her) PTSD”, and she has stopped using car-sharing altogether.

On why excess fees are so high, BlueSG said the fees are determined based on the insurers it works with — and that it has lowered excess amounts this year by about 40 per cent for both experienced and inexperienced drivers.

GetGo said its excess rates “reflect in part the cost of repairing the vehicles and resolving third-party claims”. It added: “These rates are generally in line with industry rates.”

To help users, GetGo provides the option of buying a Collision Damage Waiver at a cost of 5 per cent of the total booking charge. This reduces the excess by 50 per cent.

Tribecar, meanwhile, provides a “proprietary motor insurance excess rider”, TribeShield, which caps the excess at S$500 in the event of an accident. It goes for an additional charge of S$1.20 per hour and is capped at S$10.

UNLICENSED USERS?

One group of drivers whom car-sharing insurance will not cover are those without a licence. While registration with car-sharing platforms is required, along with a valid driving licence, unlicensed users have been caught and have ended up in court.

The companies do take steps to verify the users’ identity, and the instances where the system is abused “seem to be the minority”, said Wang Ying Shuang, deputy head of insurance and reinsurance in law firm Rajah and Tann.

But with the rise of car-sharing, there has been an increase in these offences and instances of repeat offenders, said Thomas Kapeller, the group head of insurance in fintech firm Hyphen Group.

The increase … has been notable in the last one to two years.”

There are complications when these users are involved in a road accident, as motorist Alan Teo is finding out after he was in a chain collision last month.

He told Talking Point the accident was caused by a GetGo user who had no driving licence but had booked a car with a parent’s licence.

In this “unenviable and difficult situation”, said Wang, the victim may have to make a claim on his insurance rather than be compensated by the third party, which might increase his premium upon renewal.

If the insurer can recover damages from the car-sharing user or service operator, then it may not affect the victim’s no-claim discount. But recovering damages from the user may prove difficult, depending on the quantum of the claim, she added.

It may also be difficult to attribute liability to the service operator. And the company’s insurer has discretion and the right to not cover any damages, as driving without a licence would be outside the company’s insurance cover, said Kapeller.

Car-sharing companies said they have stepped up their measures to verify that only qualified drivers can book and drive shared cars.

GetGo has implemented biometric identity verification in its app, which requires both new and existing users to submit a selfie that is then cross-checked with biometric records prior to the commencement of the booking, cited chief executive Toh Ting Feng.

The company has also developed an anti-fraud model that identifies potential fraudulent behaviours, “which will then trigger additional verification measures and/or account suspension”.

At Tribecar, user details are cross-checked against copies of the identity card or driving licence, with proof of residence required for additional verification.

Once a user is authenticated, said a spokesperson, “we regularly perform checks on the actual user”, either by comparing digital footprints and driving behaviours or by having “roaming enforcement officers” conduct checks on the ground.

Unauthorised users are given a “hefty penalty”.

This article was originally published on CNA.

No comments

Share your thoughts! Tell us your name and class for a gift (: